Understanding Flood Risk: What This Week's Flooding Means for Homebuyers

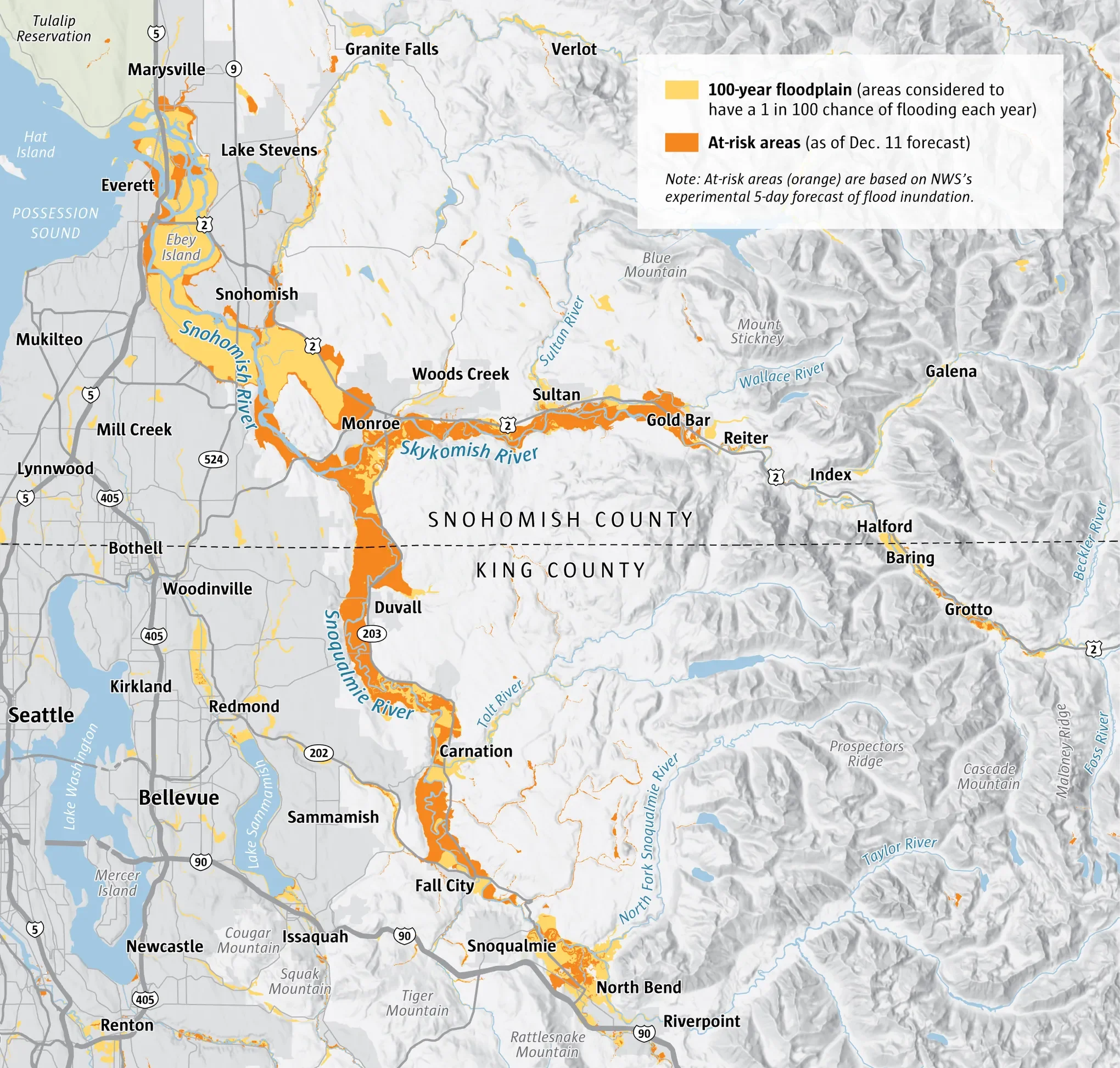

This week, Snohomish County experienced significant flooding. The Snohomish River reached record levels, leading to evacuations and widespread damage. Homes that have been safe for decades suddenly found themselves dealing with water. Roads closed. Power went out. Neighborhoods that never expected this kind of event got hit hard.

If you're looking at real estate in Western Washington, it's worth paying attention to what just happened. In the coming months, some of these properties will come back on the market. The prices might look good. The repairs might look solid. But there are things you need to understand before considering a home that's been through flooding.

What "100-Year Flood" Actually Means (And Why It Matters)

You might hear people refer to this as a "100-year flood" or see properties listed in "100-year flood zones." The term is a bit misleading. It doesn't mean a flood happens once every 100 years. It means there's a 1% chance of a flood of this magnitude in any given year.

Over the course of a 30-year mortgage, that 1% annual chance adds up to roughly a 26% probability of experiencing a major flood event. That's worth considering when you're making what's likely the biggest financial decision of your life.

The challenge is that these flood maps are based on historical data. They show us what's already happened, not necessarily what's ahead. Weather patterns are changing. Storms are getting more intense. Events that used to be rare are happening more often. It's something to keep in mind when you're evaluating long-term risk.

The Homes That Will Hit the Market Next Year

Here's what typically happens after flooding like this. Some homeowners will decide it's time to move on. They'll do repairs, get things cleaned up, and list the property. The price will often be lower than comparable homes nearby, which can look appealing.

There's also another pattern to watch for: investors who buy flooded properties, do quick cosmetic work, and flip them. Fresh paint, new flooring, updated fixtures. Everything can look move-in ready at a reasonable price. But cosmetic updates don't always address what's underneath.

Here's what's important to understand:

Hidden damage takes time to reveal itself. Water affects more than what you can see on the surface. It gets into walls, beneath floors, and into electrical systems. Mold can develop in hidden spaces. Foundation issues might not show up right away. Even with a good inspection, some problems won't surface until you've lived there for a while.

Insurance gets complicated. Once a property has flooded, insurance companies take note. Premiums can be significantly higher, and in some cases, coverage may be hard to obtain. Standard homeowner's insurance doesn't cover flooding—you need separate flood insurance through FEMA's program. Depending on the property's history and location, that can be expensive or difficult to get.

It affects resale. A documented flood event becomes part of a property's history. Future buyers, lenders, and insurers will know about it. Even with thorough repairs, it's a factor that influences long-term value and how easy the property is to sell down the road.

How to Protect Yourself

If you're house hunting in the next year, here are some steps that can help you make informed decisions:

1. Check the flood maps before you even schedule a tour.

Zillow, Redfin, and most real estate sites show FEMA flood zones. Look for them. Here's what the zones mean:

Zone X (shaded): Moderate risk. 0.2% annual chance of flooding. You're not required to have flood insurance, but you're not safe either.

Zone X (unshaded): Minimal risk. This is what you want.

Zone A, AE, AH: High risk. 1% annual chance. Flood insurance is required if you have a federally backed mortgage.

Zone V, VE: Coastal high-risk areas with wave action. Extremely high risk.

If a property is in Zone A or higher, think very carefully before proceeding.

2. Ask direct questions about flooding history.

Washington State requires sellers to disclose known material facts about a property, including flood damage. But "known" is doing a lot of work in that sentence. Ask explicitly:

Has this property ever flooded?

Has there been water damage of any kind?

What flood zone is the property in?

Is there flood insurance currently on the property, and how much does it cost?

3. Get a thorough inspection and consider additional specialists.

A standard home inspection might not catch everything. If there's any history of water issues or the property is in a flood zone, consider bringing in specialists for mold inspection, foundation assessment, and electrical systems review.

4. Run the numbers on insurance before you make an offer.

Contact an insurance agent and get a real quote for flood insurance based on the property's location and elevation. Don't assume you can afford it or even get it. This needs to be part of your buying decision, not something you figure out after you're already committed.

5. Understand what "fixed" really means.

Repairs can address visible damage, but they don't change the fundamental risk. If a property has flooded once in its location, the conditions that caused it are likely still there. The next storm will come eventually.

6. Don't assume distance from water means safety.

Properties that seem far from rivers or creeks can still be at risk. Elevation changes can be subtle. Water flows to low spots that aren't always obvious when you're driving by. A house that looks well away from the water might actually sit in a drainage path or natural low point.

The best way to understand this is to see it for yourself. Drive through neighborhoods you're considering while the effects of recent flooding are still visible. Look at which properties were affected, where streets closed, where people are still cleaning up. Talk to neighbors. They'll give you a real sense of what happened and whether it's a recurring issue.

Don't rely only on online photos or assumptions about the terrain. Go look. And if you'd like someone to come along or aren't sure what to watch for, I'm happy to drive around with you. An afternoon of observation can save you from years of problems.

The Bottom Line

I'm not suggesting you avoid Western Washington real estate. I live here, work here, and believe there are many great homes in safe areas. But recent events are a reminder to approach property decisions with care and good information.

If a property seems like an unusually good deal over the next year, take time to understand why. If it's been recently renovated by a short-term owner, ask what might be underneath those updates. Check the flood maps. Research the history. Get actual insurance quotes. Visit the neighborhood and observe what the landscape is telling you. If something doesn't feel right, it's okay to keep looking.

Buying a home is about finding a place that works for your life, not just making a transaction. Take the time to do your research, ask direct questions, and don't let a attractive price or nice finishes override concerns about location and risk. This is exactly the kind of thing that should come up in your first conversation with an agent, not after you've already fallen for a house. I wrote more about what that preparation should look like in First Home. Eyes Open. If you are considering properties in Snohomish or King County and want help understanding flood risk, I'm here to talk. I'd rather have a straightforward conversation now than see someone struggle with unexpected problems later. And if you'd like to drive around and look at areas together to get a better sense of what's at risk, I'm glad to do that. Sometimes seeing things in person makes all the difference.

Additional Resources

FEMA Flood Map Service Center - Check official flood zones for any address

Flood Smart - Government tips on insurance and what to do before and after

TIME: Why 'Hundred-Year' Storms Are Happening More Often - Climate change is making 100-year floods occur every 25 years in some areas

Yale Climate Connections: 100-Year Floods Are Happening More Often - Research on increasing flood frequency

USGS: The 100-Year Flood - Understanding what the term actually means

EPA Climate Indicators: Coastal Flooding - Data on increasing flood frequency along U.S. coasts